At a microfinance group meeting, you might see a lot of paper: piles of cash, thick record books to record attendance and meeting minutes; repayment schedules; group loan balance reports; passbooks. At the branch office, too, more paper: stacks and binders and file cabinets full of applications and loan contracts.

These documents are the by-products of best practices in microfinance. They are meant to ensure accountability and transparency. But extensive documentation processes can cost time and money for the company and clients, and a high volume of cash transactions can create security and fraud risks.

In recent years, there’s been a lot of buzz, and skepticism, about Sweden’s efforts to move to a cashless economy. Other countries are following suit. In the place of physical cash, these economies are increasingly using credit, debit, and mobile payments for financial transactions. One central criticism of cashless economies is that the reliance on technology will exclude vulnerable populations – those who are most likely to be unbanked or have low digital literacy or technology access.

What if microfinance institutions could eliminate cash and paper, and still deliver last-mile credit services?

Pioneers in the microfinance sector are harnessing leapfrog technology to do exactly this. Instead of seeing adoption of technology as a barrier for marginalized communities, these innovators are harnessing the power of digitization to expand financial inclusion.

Introducing Musoni Microfinance

Musoni Microfinance, established in Kenya in 2009, strives to provide 100% cashless and paperless services. It serves as the real-world testing ground for the Musoni System. This cloud-based core banking solution is built specifically to help microfinance organizations integrate new mobile and digital technologies to improve efficiency, reduce costs, and expand rural outreach. The interface is compatible with tablets, mobile phones, and computers. It’s built to integrate smoothly with mobile money, and to be user-friendly for clients, field officers, and senior managers.

What does this mean for Musoni’s goal? They haven’t quite eliminated paper yet. But they are getting closer and closer by focusing on entry level clients.

Whole Planet Foundation recently pledged $500,000 over three years to support the scale of Musoni’s most digitized loan product yet: the M-Nawiri group business loan product.

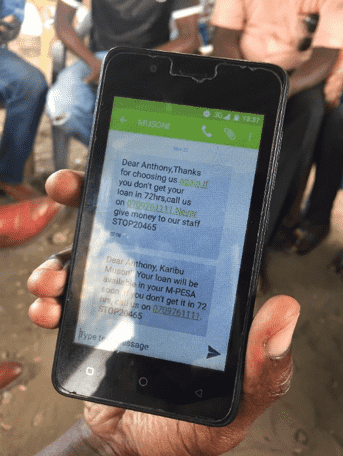

For the M-Nawiri loan, almost everything is recorded and monitored digitally. This includes client profile details; loan applications and approvals; credit history; repayment schedules; repayment reminders. At the group meetings I visited I often saw just two physical documents: The group members brought a record book, where they keep track of all group meetings and minutes; and the loan officer brought a one page print out of the group’s loan balance. There was no physical cash on the table; repayments were all made through mobile money which then directly posts to the loan account.

At one group meeting, the members approved a loan to a new member. The loan officer and other members helped the new client go through the USSD menu on her own simple feature phone to fill out the loan application. This information directly feeds into Musoni’s database, which already contained her profile and registration details. This type of digital integration is present in all aspects of the loan process, from registration and application to approval, disbursement, and repayment.

As the microfinance industry becomes increasingly digitized, more and more institutions are adopting tools to help streamline tasks. Many have gone a step further, by using fully digitized, algorithm based mobile money loans in which there’s no direct in person contact between the borrower and the bank. The allure of relying more on technology is understandable: wider outreach and scalability without the costs of a physical presence. But often, these loans sacrifice too many know-your-client best practices, resulting in high levels of default and client over-indebtedness.

Photo courtesy of Musoni Microfinance.

This trend is especially apparent in Kenya, the birthplace of mobile money. An estimated 90% of Kenyans own mobile phones and 52% of the total population uses mobile money. Mobile money has been a significant driver of financial inclusion in Kenya. As of 2017, 82% of Kenyan adults held some form of financial account; roughly 25% of Kenyans held only a mobile money account. The growth of mobile money has been accompanied by a growth in financial services. The ease of sending and tracking money has led to a recent boom in services providing quick, near-instant mobile loans. This surge in credit options has also led to what some call a crisis in over-indebtedness, characterized by poor transparency and irresponsible lending behaviors especially affecting poorer borrowers.

In this context, Musoni’s M-Nawiri loan uses technology to replace paper and money, but it also steadfastly retains many of the aspects of a more traditional microfinance methodology. Business and home visits, group solidarity, and frequent group meetings are all integral to their loan process. Musoni remains committed to high touch, client centered services despite the competitive pressures in the market.