During this year’s Financial Inclusion Week, Accion’s Center for Financial Inclusion asks, “Financial Inclusion for What?” In other words, what are the main goals that financial inclusion is striving to achieve?

Whole Planet Foundation (WPF) has been a unique capital provider in the financial inclusion space for almost 15 years. The foundation provides free capital to many organizations that are operating sustainably. Therefore, WPF selects partners with a strong social focus in terms of the implementation of financial services and other services that can be delivered to clients by leveraging their field-based microcredit programs. WPF evaluates partners on their ability to provide accessible, transparent/affordable and supportive services to their clients.

In Accion’s framework – this would translate to:

-

- Financial inclusion for financial health

- Financial inclusion for equity

- Financial inclusion for sustainable development.

CASHPOR: A Case Study

Earlier this month I visited with one of WPF’s India partners, CASHPOR. They are an excellent model for the types of Microfinance Institution (MFI) that can leverage WPF capital in an extremely effective way towards these three targets.

Financial Inclusion for Financial Health

“Fundamentally, financial tools exist to help people manage mismatches between their income and expenses over time and space and build lump sums of cash. The ability to do those things is financial health.”

In the Indian context, there is no shortage of credit providers who are willing to offer loans. CASHPOR has taken the approach under their New Growth Strategy to finance the full, legitimate capital needs of their borrowers. In return, the borrowers are asked to borrow exclusively from CASHPOR. This strategy recognizes that clients have both business credit needs as well as family credit needs (like school fees, marriages or illnesses) that require access to lump sums. CASHPOR’s flexibility in amount and purpose of their microloans allows borrowers to manage their cash flows, take advantage of business opportunities and respond to emergencies. CASHPOR gives the loans in full context of the entire family’s repayment capacity and by working exclusively with CASHPOR, the risk of over-indebtedness which is associated with multiple borrowing can be decreased.

Financial Inclusion for Equity

Microfinance institutions “should be striving for equity – fair access, fair use and fair treatment for customers – but where do we focus our efforts?” These first two ideas of financial health and financial equity are very closely linked for an organization like CASHPOR. It is impossible even to describe CASHPOR’s provision of financial services to smooth capital needs without discussing how they are providing capital in a responsible way. These two goals are fundamentally linked.

In terms of fair access, it is significant as well to look at CASHPOR’s target population. They work in 5 of the poorest states in India. Within these states, they focus on rural areas and use tools such as the CASHPOR Housing Index to specifically prioritize Below Poverty Line (BPL) households. According to CASHPOR’s stats almost 90% of members are from “scheduled castes, scheduled tribes or other backward classes.”

CASHPOR client, Indrawati, and her two daughters.

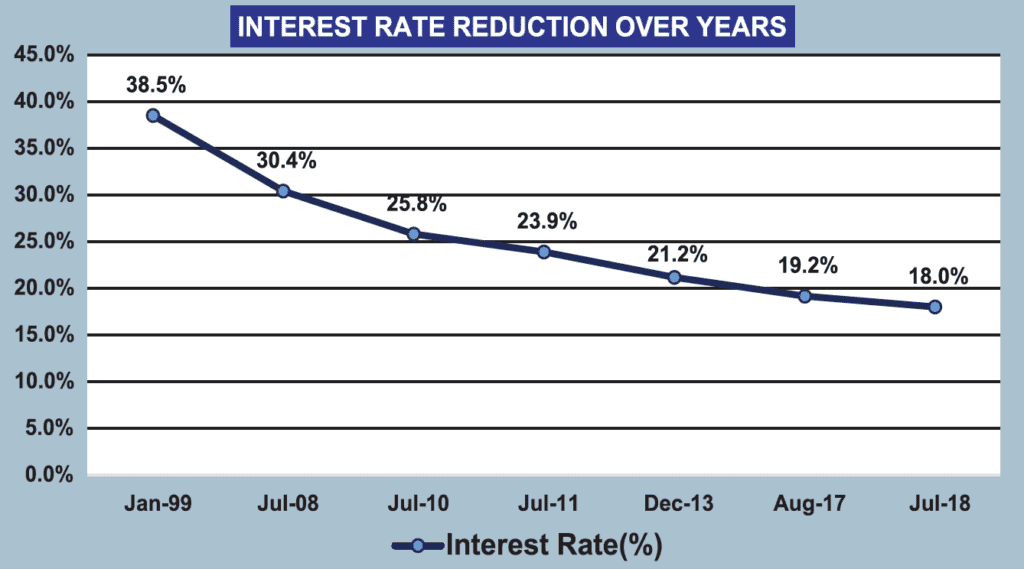

In terms of usage, CASHPOR strives to offer the lowest interest rates in the areas which they serve. Fair treatment of customers is taken especially seriously by the CASHPOR staff. While most WPF partners make a point to print branch and regional staff phone contacts on passbooks or even have a head office hotline where complaints can be filed, CASHPOR goes even further to have a “Client Satisfaction Day.” On the 15th of every month, clients are encouraged to visit the branch office and discuss any concerns/feedback they have.

Financial Inclusion for Sustainable Development

“Financial inclusion, financial services, and microfinance are explicitly mentioned in the targets of seven of the 17 Sustainable Development Goals. Their presence implies that financial services are a means to improve quality of life and suggests that creating financial stability should not be the only goal of financial inclusion.”

Indeed, CASHPOR’s vision and mission go beyond providing financial services but also to deliver health and education services as approaches to break the intergenerational poverty cycle for the clients they serve. CASHPOR leverages its rural network to provide access to these services. One key to CASHPOR’s health and education initiatives is a team of more than 3,000 Community Health Facilitators which cover about 95% of CASHPOR’s centers! These are CASHPOR clients who have gone through intensive training and internship in partnership with Healing Fields Foundation and now deliver health modules to their fellow clients. CHF’s also take on additional roles in the organization regarding promoting health related loans and monitoring educational activities that keeps these programs scaled across the large organization.

A health catastrophe can be a big setback to a low-income client. CHF’s leverage the fact that clients come together on a weekly basis for their credit and saving activities to deliver preventative trainings. CHF’s also sell health-related items like insect repellent and sanitary napkins. And they promote products such as the sanitation loan, in which CASHPOR will provide financing for the construction of a toilet at the client’s home. CASHPOR also leverages its rural branches to deliver Mini Health Clinics where doctors visit twice a month to provide consultations and medicine. As of March 2019, 177 CASHPOR branches held mini-health clinics, serving almost 134k clients.

While a health catastrophe can send a rising client back into poverty, educational opportunities are a strong way to propel a family forward. CASHPOR’s specific goal is that every family should have at least one child pass the grade 10 exams, which unlocks the possibility for government jobs. To this end, CASHPOR has partnered with an NGO named PRATHAM to develop Education Centers where students can get tutoring before or after regular school hours. CASHPOR has established 1,092 CASHPOR Educational Centers which serve over 33k students. As of most recently available info, 93% of the CEC students who sat for the class 10 exam in Bihar and Uttar Pradesh have passed. Clients pay a small amount for participation in the education centers and/or health clinics in order to recoup some of the costs and continue to scale the programs. The CHF’s earn stipends from CASHPOR for their work.

Historically, subordinated debt and grant capital from donors like WPF reinforce CASHPOR’s capital which in turn unlocks their ability for further borrowing. As CASHPOR has become more sophisticated, they can expand their program directly by employing funds from their banking correspondent partners to entire branches. However, fresh funds from WPF can be leveraged for the riskier expansion areas where CASHPOR has to go with their own funds. Because of the non-profit structure, income earned from interest is all reinvested back into the organization – helping CASHPOR to continue to expand the financial and non-financial services. And operational efficiencies are shared back with clients through reducing interest rates over time. (And this last year – an interest refund to veteran clients!)

Whether large or small, WPF seeks out partners with responsible finance practices and the ability to use WPF funds in an impactful way. In addition to supporting traditional socially focused MFI’s like CASHPOR, WPF’s mandate also incorporates other innovative approaches such as the Ultra Poor graduation framework and social enterprises providing clean energy and health products on credit.